CBS News Live

CBS News Bay Area: Local News, Weather & More

Watch CBS News

Breaking Local News, First Alert Weather & Community Journalism

Instead of telling people to wait for the light to change colors, there were AI-generated messages impersonating Meta CEO Mark Zuckerberg and Tesla CEO Elon Musk.

With just days remaining before Tuesday's special election, Oakland mayoral candidates Barbara Lee and Loren Taylor spent the weekend canvassing neighborhoods across the city, urging residents to turn in their ballots amid what officials are calling alarmingly low voter turnout.

They say necessity is the mother of invention and in Petaluma, two mothers are teaming up to invent a new kind of coffee shop and it's happening in a most unlikely location.

Rory McIlroy won a sudden-death playoff to finally win the Masters and take his place in golf history as the sixth player to claim the career Grand Slam.

James Harden hit consecutive 3-pointers in overtime, a pair of free throws and scored on Jimmy Butler's goaltending to finish with 39 points and 10 assists, Kawhi Leonard scored 33, and the Los Angeles Clippers secured the fifth seed in the Western Conference playoffs by beating the Golden State Warriors 124-119 in the teams' regular-season finale.

An investigation is underway after a body was found burned near Vacaville Sunday morning, deputies said.

Jung Hoo Lee homered in consecutive at-bats off Carlos Rodón, and the visiting Giants rallied from a three-run deficit to beat the Yankees 5-4 Sunday.

Berkeley Police said they shot an armed suspect who walked out of a home where a woman was heard yelling for help Sunday morning.

President Trump underwent the physical on Friday at Walter Reed Hospital.

With just days remaining before Tuesday's special election, Oakland mayoral candidates Barbara Lee and Loren Taylor spent the weekend canvassing neighborhoods across the city, urging residents to turn in their ballots amid what officials are calling alarmingly low voter turnout.

President Trump underwent the physical on Friday at Walter Reed Hospital.

Sen. Bernie Sanders, who had a rally earlier in Los Angeles, urged young people to "stand up and fight" at the music festival.

On Tuesday, Oakland voters will head to the polls to elect a new mayor following a recent recall — but the high-stakes mayoral race isn't the only item on the special election ballot.

President Trump justified the use of the military by saying the United States is "under attack from a variety of threats."

Rory McIlroy won a sudden-death playoff to finally win the Masters and take his place in golf history as the sixth player to claim the career Grand Slam.

James Harden hit consecutive 3-pointers in overtime, a pair of free throws and scored on Jimmy Butler's goaltending to finish with 39 points and 10 assists, Kawhi Leonard scored 33, and the Los Angeles Clippers secured the fifth seed in the Western Conference playoffs by beating the Golden State Warriors 124-119 in the teams' regular-season finale.

Jung Hoo Lee homered in consecutive at-bats off Carlos Rodón, and the visiting Giants rallied from a three-run deficit to beat the Yankees 5-4 Sunday.

J.T. Ginn allowed one run in five-plus strong innings and the Athletics beat the New York Mets 3-1 on Saturday for their second home win since relocating to West Sacramento.

The Yankees beat the San Francisco Giants 8-4 on Saturday.

The San Francisco Embarcadero is full of eye-catching destinations: from Fisherman's Wharf, Pier 39, the Exploratorium, and the iconic Ferry Building to name just a few iconic stops.

With thousands of plant and animal species, including dozens found nowhere else on Earth, Catalina is a world-class diving destination. Yet scientists warn this underwater paradise faces a growing threat.

At the edge of the Arctic in northern Canada, the annual migration of polar bears draws tourists, photographers, and scientists like Geoff York.

Plastic waste is a huge problem, with bags and packaging a major culprit. A Bay Area startup has figured out a way to replace these plastics, with a plant that grows abundantly off the coast.

Petaluma's experiment with reusable cups last fall was a resounding success according to a newly released report on the project.

The widespread destruction of old growth trees for ranching and farming is making it harder to get the wood traditionally used to make guitars, including mahogany and Brazilian rosewood.

In San Francisco's Dolores Heights, an unusual design and branding studio is the home of two creative artists who earned a Grammy nomination for their groundbreaking album artwork.

President-elect Donald Trump promises to "unleash American energy" by maximizing U.S. oil and gas production. The directive comes at a time when the planet continues to warm, largely due to the burning of fossil fuels, experts say.

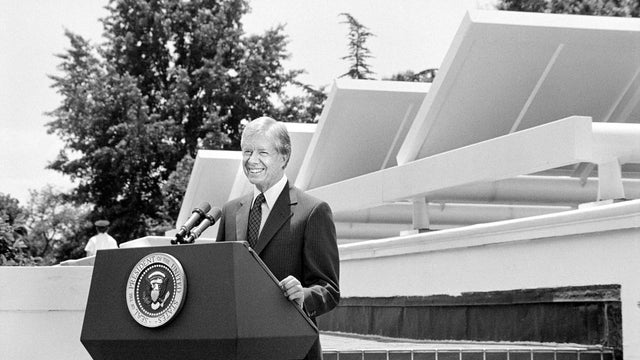

When it came to protecting Mother Earth, in many respects, the late President Jimmy Carter was way ahead of his time.

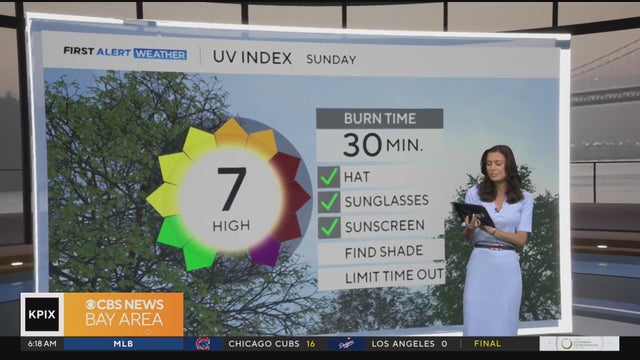

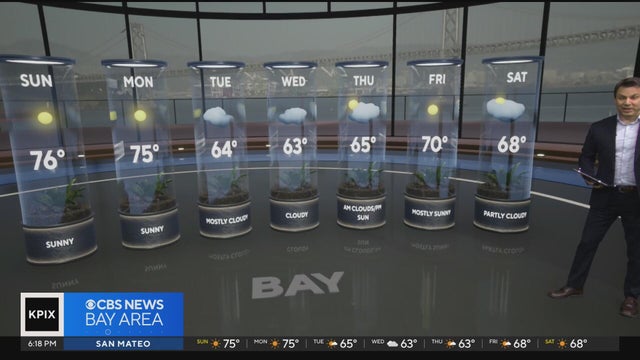

Here's a look at the weather forecast.

with Zoe Mintz.

Here's a look at the weather.

with Zoe Mintz.

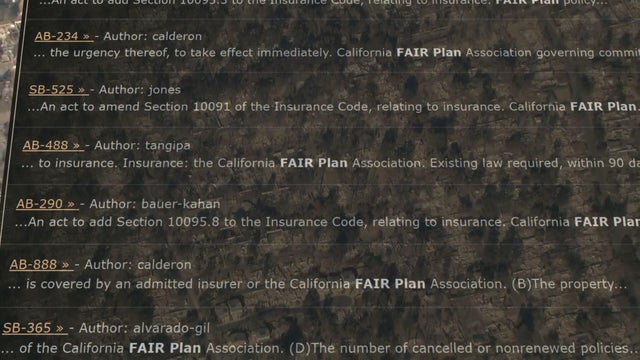

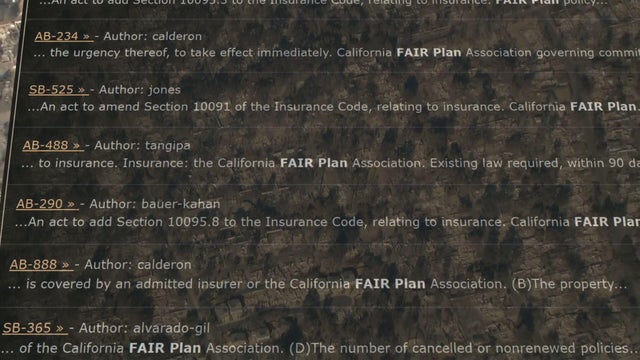

FAIR plan problems are nothing new, but suddenly, everyone is paying attention to California’s insurance crisis. Are we any closer to a fix? CBS News California investigates the flood of insurance-related bills in the aftermath of the L.A. fires and why it’s taken so long for lawmakers to take action.

FAIR plan problems are nothing new, but suddenly, everyone is paying attention to California's insurance crisis. Are we any closer to a fix? CBS News California investigates the flood of insurance-related bills in the aftermath of the L.A. fires and why it's taken so long for lawmakers to take action.

As more people in California lose private insurance, the state's FAIR plan is filling up with homes in places the industry itself has classified as low-risk for wildfire.

Instead of telling people to wait for the light to change colors, there were AI-generated messages impersonating Meta CEO Mark Zuckerberg and Tesla CEO Elon Musk.

Here are the latest headlines.

Former Communications Director of Oakland Mayor Justin Berton joined the show to discuss they city's upcoming special election.

Here's a look at the weather forecast.

They say necessity is the mother of invention and in Petaluma, two mothers are teaming up to invent a new kind of coffee shop and it's happening in a most unlikely location.

CBS News Bay Area anchor Elizabeth Cook talks with USF professor of law and migration studies Bill Ong Hing about the positions of the Trump and Harris campaigns when it comes to immigration reform and the situation at the border

CBS News Bay Area anchor Elizabeth Cook asks UC Berkeley Haas School of Business professor Olaf Groth, PhD, about how AI could play a role in potential election interference

CBS News Bay Area anchor Anne Makovec asks UCSF infectious disease specialist Dr. Monica Gandhi if Covid is any more serious than a cold these days, the latest on long Covid, and if the bird flu poses any threat of becoming the next pandemic

The race for the White House is flooding our feeds. CBS News Bay Area anchor Anne Makovec asks Dr. Nolan Higdon with CSU East Bay about the impact of influencers in the presidential race, and if they can really tip the scales in battleground states

CBS News Bay Area anchor Anne Makovec hears from Niku Sedarat from San Jose, an incoming Stanford student and member of DoSomething.Org, about an initiative that allows students to share ideas about addressing mental health in their communities. Anne also asks Dr. Nicole Stelter from Blue Shield of California how parents can provide support for their children

CBS News Bay Area anchor Elizabeth Cook has been reporting extensively on the rise in lung cancer cases among non-smoking Asian American women. Now, Liz talks to a Bay Area mother whose trip to Kaiser Permanente Oakland Medical Center after a car crash may have saved her life. Liz also talks to Dr. Jeffrey Velotta, who performed the surgery, about the rise in lung cancer cases in Asian American women and what may be causing them

CBS News Bay Area anchor Elizabeth Cook talks to Coalition on Homelessness Executive Director Jennifer Friedenbach and Senior Vice President of Public Policy for the Bay Area Council Adrian Covert to hear both sides of the debate over Gov. Newsom's executive order to clear homeless encampments

Vice President Kamala Harris has announced her bid for the White House and has appeared to fend off any challengers for the Democratic nomination. CBS News Bay Area anchor Elizabeth Cook asks UC Berkeley Haas School of Business professor Olaf Groth, PhD, which candidate will get support from Silicon Valley

Andrea Nakano and Brian Hackney spoke to San Jose State senior lecturer Donna Crane and Sonoma State professor David McCuan about the stunning developments in the presidential race Sunday. (7-21-24)

San Francisco City Attorneys are trying to close four Tenderloin businesses that they say have been operating as illegal casinos and trading spots for drugs and stolen merchandise.

On Saturday, San Francisco officials celebrated the opening of the newest city park on what used to be the Great Highway next to Ocean Beach.

In May of last year, an Italian restaurant and market opened on Clement, a street that's already lined with restaurants. In a short amount of time, it's won over many regulars.

Instead of hitting the road, 33-year-old Stephanie Cowan hit "send" from the backseat of an electric SUV parked smack dab in the middle of a car dealership.

The San Francisco Embarcadero is full of eye-catching destinations: from Fisherman's Wharf, Pier 39, the Exploratorium, and the iconic Ferry Building to name just a few iconic stops.

With just days remaining before Tuesday's special election, Oakland mayoral candidates Barbara Lee and Loren Taylor spent the weekend canvassing neighborhoods across the city, urging residents to turn in their ballots amid what officials are calling alarmingly low voter turnout.

Berkeley Police said they shot an armed suspect who walked out of a home where a woman was heard yelling for help Sunday morning.

On Tuesday, Oakland voters will head to the polls to elect a new mayor following a recent recall — but the high-stakes mayoral race isn't the only item on the special election ballot.

A proposal would require Berkeley homes between Tilden Park and Panoramic Hill to remove foliage within 5 feet of the home as a wildfire prevention measure.

Relief rippled through Oakland's Montclair District on Friday as police announced the arrest of three individuals connected to a violent daytime robbery and shooting that rocked the normally quiet neighborhood.

Instead of telling people to wait for the light to change colors, there were AI-generated messages impersonating Meta CEO Mark Zuckerberg and Tesla CEO Elon Musk.

Northern Santa Clara is transforming an old manufacturing hub into a bustling neighborhood that promises to bring in new business and entertainment zones.

The City of San Jose and the San Jose Quakes are sponsoring a 10-week pilot program aimed at giving middle school and high school kids more opportunities in sports.

The United States will open the CONCACAF Gold Cup against Trinidad and Tobago on June 15 at PayPal Park in San Jose.

Two suspects have been arrested in connection with a deadly shooting of a 19-year-old man in San Jose in February, police said.

They say necessity is the mother of invention and in Petaluma, two mothers are teaming up to invent a new kind of coffee shop and it's happening in a most unlikely location.

A new art exhibit titled "The Only Door I Can Open" is offering the public a rare, intimate glimpse into the realities of incarceration, curated by formerly and currently incarcerated artists—many of whom developed their talents inside San Quentin State Prison.

A shelter in place order for a Novato neighborhood was lifted Wednesday night following a three-hour search to find juveniles allegedly involved in a shooting.

Authorities in Sonoma County said a Santa Rosa man suspected of possessing child pornography was arrested Wednesday on suspicion of animal cruelty for sexual assaulting a small dog.

A long-running and unusual theater tradition in the North Bay is in jeopardy of coming to an end due to budget challenges.

After multiple times repainting her storefront only for it to be graffitied again the next day, one store owner said she gave up trying to keep it clean.

Sunset Dunes will be the name of San Francisco's newest park, located on part of the now-closed Upper Great Highway.

A San Francisco park ranger is being recognized by the city for her work helping homeless residents who live in Golden Gate Park.

A long-awaited bridge project is underway in the North Bay, but construction has created a situation residents said is a "safety" issue.

The visas issued to six students at both UC Berkeley and Stanford were revoked by the federal government in the past week, according to campus officials.

Instead of telling people to wait for the light to change colors, there were AI-generated messages impersonating Meta CEO Mark Zuckerberg and Tesla CEO Elon Musk.

With just days remaining before Tuesday's special election, Oakland mayoral candidates Barbara Lee and Loren Taylor spent the weekend canvassing neighborhoods across the city, urging residents to turn in their ballots amid what officials are calling alarmingly low voter turnout.

They say necessity is the mother of invention and in Petaluma, two mothers are teaming up to invent a new kind of coffee shop and it's happening in a most unlikely location.

Rory McIlroy won a sudden-death playoff to finally win the Masters and take his place in golf history as the sixth player to claim the career Grand Slam.

James Harden hit consecutive 3-pointers in overtime, a pair of free throws and scored on Jimmy Butler's goaltending to finish with 39 points and 10 assists, Kawhi Leonard scored 33, and the Los Angeles Clippers secured the fifth seed in the Western Conference playoffs by beating the Golden State Warriors 124-119 in the teams' regular-season finale.

Kennedy's comment comes as the Environmental Protection Agency says it has now launched a new review of fluoride's health effects.

A fire involving a portable air compressor at the Martinez Refining Company on Wednesday night left one person injured, according to officials.

Tony's Chocolonely is recalling some products after consumers reported finding "small stones" in the chocolate bars.

A University of California, Berkeley student has created an artificial intelligence startup to help people detect strokes and other medical emergencies and will be taking part in an innovation competition on Wednesday, the university said.

As mass layoffs commenced nationwide for Department of Health and Human Services workers, one employee seen leaving the Nancy Pelosi Federal Building in San Francisco Tuesday morning said she was "devastated" and "heartbroken."

An investigation is underway after a body was found burned near Vacaville Sunday morning, deputies said.

Berkeley Police said they shot an armed suspect who walked out of a home where a woman was heard yelling for help Sunday morning.

San Francisco City Attorneys are trying to close four Tenderloin businesses that they say have been operating as illegal casinos and trading spots for drugs and stolen merchandise.

Three people were shot at Davis' Community Park on Saturday as crowds gathered in the city for Picnic Day, police said.

Relief rippled through Oakland's Montclair District on Friday as police announced the arrest of three individuals connected to a violent daytime robbery and shooting that rocked the normally quiet neighborhood.

Ever since the COVID-19 pandemic, the Oakland Unified School District has seen an alarming spike in the number of unhoused students in the school system who deal with a host of challenges far beyond what most children face.

Meteorologist and CBS News Bay Area's resident pilot Lt. Jessica Burch got a treat during Fleet Week, taking to the skies with one of the Blue Angels.

A Bay Area man discovered his devastating loss left him with a new opportunity to rethink how he lives -- follow his journey in virtual reality, 360-degree video.

A groundbreaking medical study involving the UCSF Medical Center has shown some colorectal cancer patients can safely skip radiation treatment and enjoy a potentially higher quality of life.

Every day, San Francisco bar pilot Captain Zach Kellerman goes through what might just be the world's most dangerous commute.

The Trump administration is gearing up to investigate schools for potential Title IX violations for allowing transgender women to compete in women's sports, including San Jose State.

The NCAA updated its policy one day after the administration's order banning transgender athletes from competing on female teams.

The order directs that federally-run insurance programs, including TRICARE and Medicaid, exclude coverage for gender-affirming care for those under 19.

A Milpitas man convicted in the 2021 domestic violence murder of his transgender partner has been sentenced, prosecutors said.

John Ramos reports on how transgender advocates reacted to President Trump's announcement the government would only recognize two genders.

It happened several days after Halloween, but composer and former Oingo Boingo frontman Danny Elfman delivered an appropriately macabre set of movie soundtracks and '80s hits for a full house at the Shoreline Amphitheatre.

Bay Area pop-punk heroes Green Day brought their current Saviors Tour to Oracle Park in San Francisco Friday for an epic show that also featured alt-rock favorites Smashing Pumpkins and fellow punk acts Rancid and the Linda Lindas.

An all-star group featuring King Crimson members Adrian Belew and Tony Levin along with guitar giant Steve Vai and Tool drummer Danny Carey played the music from Crimson's '80s albums at the Meritage Resort and Spa in Napa Friday.

Grammy-winning country-blues songwriter Lucinda Williams and her band put on a show-stopping performance at Stern Grove in San Francisco on Sunday, Aug. 18.

This year's edition of Outside Lands came to an eclectic close Sunday with sets from headliner Sturgill Simpson, rising star Chappell Roan, rapper-turned-country-singer Post Malone and more.

In 2025, KPIX is moving to a new community service award: the CBS News Bay Area Icon Award. Submit nominations for an outstanding community hero at kpix.com/icon.

It's the most wonderful time of the year for a South Bay woman who has played Mrs. Claus for more than 40 years for the children of North San Jose's Alviso District.

For residents of the Oakland Hills, the prospect of another wildfire always remains a concern. This week's Jefferson Awards winner has made it his mission to make the hills and other high-risk areas safer.

In East Palo Alto -- where state education numbers show more than nine in ten public school students are low income and more than half are English learners -- many are finding hope and connection at the Boys & Girls Clubs of the Peninsula.

This week's Jefferson Award winner is Army veteran who continues to live a life of service into his 80s, by feeding hundreds of San Francisco families a week.

A Bay Area man who overcame tremendous obstacles to excel in school has made it his mission to gear up other students for success in the classroom and in life.

For Students Rising Above scholar Josh Collins it took moving across the country to realize the value of his Bay Area family.

Samir Hooker had to grow up fast after his stepfather was shot dead 12 years ago. Now he is watching over his mom and sister while attending UC Berkeley.

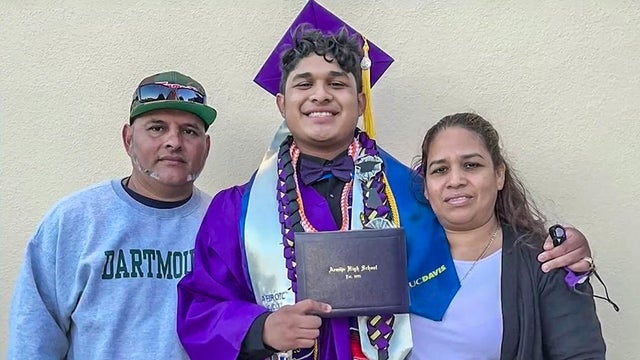

It's hard enough to graduate from one of the most prestigious schools in the country when you're the first in your family to go to college. Imagine doing that while you're also trying to protect your parents from being deported?

Some students who are the first in their families to go to college face the challenge of balancing a rigorous academic load while still working to help support their family back home.